Cement producers are in the climate cross-hairs, as the sector is responsible for 8% of global carbon dioxide emissions. Regulatory and commercial pressure is growing to cut these emissions, drastically and fast. There are no easy options available and many uncertain and unproven technologies, all of which claim to be the silver bullet. So what on earth should a producer do?

A raft of different new technologies are available to consider; from the use of artificial intelligence (AI) for energy optimisation, to carbon capture, graphene and green hydrogen, the choice can seem bewildering. But many solutions are still only on the horizon and can’t yet be deployed at scale.

And it’s now that action is needed. Research published in Nature in 2021 said achieving large emissions reductions by 2030 – without ever reaching net zero – delivers a significantly better climate result than reaching net zero through a big improvement between 2040 and 2050. Not forgetting, of course, that reducing carbon emissions sometimes can reduce operating costs.

Carbon Re has taken a closer look at 20 technologies making claims to decarbonise cement production. We discounted 7 of them completely as they just aren’t able to move from the lab into the real world in time for 2030. We then modelled the remaining 13 that we believe have the potential to make an impact within the next decade. We assessed the potential of each technology to reduce carbon emissions by 2030 – and the expected costs of each technology.

What we found was that these 13 technologies could reduce emissions in cement production from 2.5 Gt CO2 in 2022 down to 1.7 Gt CO2 in 2030. This is over double the reduction targeted by the International Energy Agency and equivalent to the total annual greenhouse gas emissions of the United Kingdom and France, combined.

And of these, our research found that five technologies already well known to the cement industry – and all of which are scalable – have the potential to provide more than 80% of the reduction in carbon emissions needed by 2030. The five technologies in question fall into three groups:

-

Substitute cementitious materials (SCM) – including LC3 cement, which is based on a blend of limestone and calcined clay

-

Biomass and waste-derived alternative fuels

-

AI for energy efficiency and SCM blending

Our latest white paper, Three technologies to reduce climate change, examines these in greater detail, but it’s also worth taking a look in more depth at some of the technologies that are getting a lot of attention, but which are less able to deliver short-term results.

Hydrogen

Seemingly highly regarded solutions such as green hydrogen, may end up having less impact than expected when a holistic view is taken. Cement production using green hydrogen is not the most efficient use of renewable electricity. The efficiency losses that occur at each stage of the process in conjunction with the significant demand from other industries means green hydrogen prices will be high. Adding in the difficulty to implement due to the new infrastructure required and lack of commercial suppliers, and the viability for green hydrogen in cement production is significantly decreased.

Waste Heat Recovery

While waste heat recovery is a mature, commercially available technology with multiple suppliers, the capital investment required and the resulting cost of the electricity generated limits its benefits. Moreover, not all cement plants are suitable for waste heat recovery. Newer and more efficient cement plants won’t benefit enough from this technology.

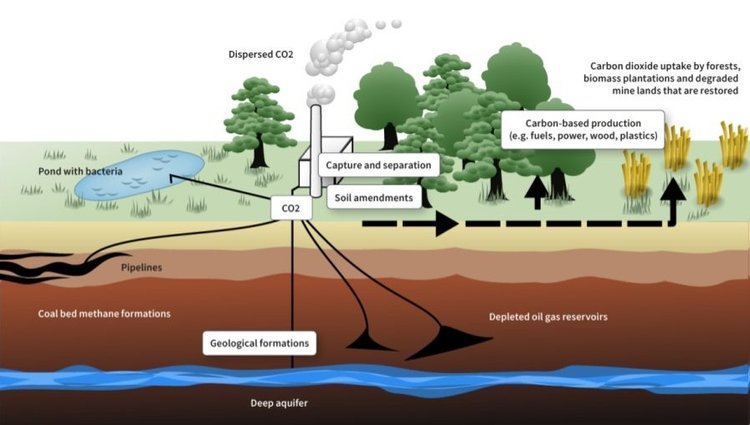

CCUS

Carbon Capture, Utilisation and Storage (CCUS) is the technology of containing CO2 emissions that would otherwise be released into the atmosphere, and then either locking the gases away or using them in some beneficial way. While there are no industrial scale projects yet, it is not new. Pilot projects have been undertaken for decades. Which is precisely the problem, although CCUS is seen as the only way to address the carbon emitted during cement production from the chemical reaction when limestone becomes clinker, it is yet to be proved at scale. What’s more, capital investment and operating costs for CCUS are significant. They are predicted by industry experts to more than double the price of cement.

Even though the technologies we’ve mentioned here may not be ready to deploy at scale now, cement producers should still have them on their roadmap. Ultimately, if the sector is going to reduce emissions, it needs to leverage every opportunity and technology available, whenever possible.

We would just encourage producers to prioritise the solutions that are most practical and will deliver the biggest impact today.